Jobber

Academy

Expert advice, entrepreneur success stories, best practices, and tools to run smarter, more efficient service businesses.

8 Best Scheduling Apps for Small Business Owners

10 Simple Ways to Increase Revenue From Existing Customers

How to Build a Customer Referral Program That Wins More Clients

10 Easy Ways to Increase Revenue From New Customers

Yes, You Need a Business Bank Account. Here’s How to Set One Up

How to Attract More Customers With Google Reviews

How to Ask For a Review [With Free Templates]

How to Respond to a Negative Review: Response Examples & Templates

Reconnecting With Old Clients Email Template: The Ultimate Guide

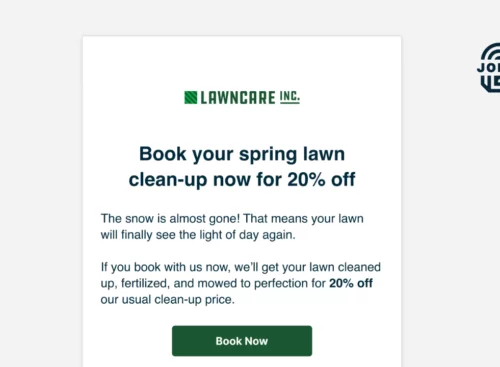

Email Campaign Examples and Tips to Upgrade Your Marketing

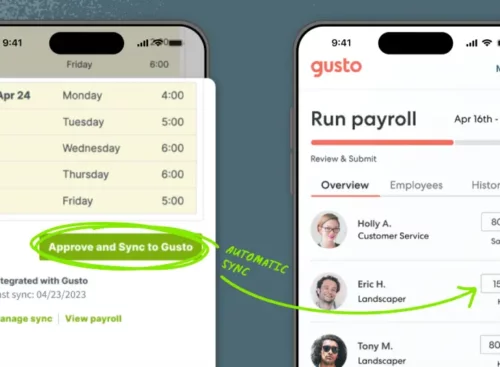

Best Payroll for Small Business: Top 8 Software Solutions